15 Oct 2024

Indonesia looks to pick up a little steam as well next year, though it will need to heed the pitfalls of easy choices and fiscal slippage to make gains stick for the long term. Things are also ticking up in Thailand, as a new government gets to work, and the tourism recovery continues apace. Malaysia is riding the wave of inward investment, though growth may cool at the margin over the coming year. Singapore, meanwhile, is chugging along, with its growth so far this year better than hoped, though slower global trade could soon add a little drag. The Philippines is taking a little breather this year, before revving up again in 2025 as inflation tumbles and spending power increases. Vietnam has overcome its dip in growth, helped by a robust external sector, while local demand is reviving.

Key upcoming events

Following the election in February, the General Election Commission (KPU) announced in March that Prabowo Subianto has won an outright majority, garnering 58.6% of the votes, and is set to be Indonesia’s next president, starting on 20 October. All eyes are now on the key people and policies the new government champions. The continued presence of technocrats in key ministerial posts would signal a desire to push ahead with reforms, and the final legislative count will determine the parliamentary muscle power behind potential reforms.

Prabowo has spoken at length about continuing current President Jokowi’s reforms – embarking on down-streaming 2.0 and continuing the infrastructure build-out. However, we believe there will be challenges along the way: for instance, slower global demand for nickel electric vehicle (EV) batteries, lowering Indonesia’s carbon footprint, and restructuring certain state-owned enterprises (SOEs). Prabowo has outlined plans to upgrade defence systems and enhance social welfare schemes (in particular a new free lunch programme at schools). The challenge is to keep a lid on the fiscal deficit and hold on to Indonesia’s well-maintained macro stability over the next five years.

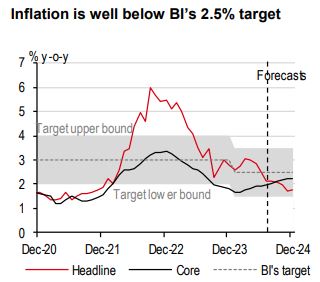

We do believe that a decade of reforms has put in place several buffers that would help keep the house in order, at least in the short term. For instance, better infrastructure and lower logistics costs will likely keep a lid on core inflation, as has been clear in recent months. Supply-side reforms could help further control the rise in food inflation. And rising exports of processed metals will likely keep the external deficits manageable.

For now, however, growth is rather weak. Q2 GDP was 7.8% below pre-pandemic trend levels. The contraction in July and August PMIs suggest that activity weakened into Q3. As Bank Indonesia (BI) cuts rates, the new government takes over and announces its vision, thereby lowering policy uncertainty, and FDI inflows waiting on the side-lines flow in, we believe growth prospects could improve. We expect GDP growth to rise from 5% in 2024 to 5.3% in 2025 and 2026.

Our growth model suggests that switching to loose fiscal and monetary policy could help raise growth, but only partially. Moving further up the manufacturing value chain, and graduating from exporting just ores and metals, to exporting EV batteries and EVs, and thereby reducing the impact of commodity price shocks on the economy, could push potential growth to 5.8% by 2028.

After slow growth in 2023, Malaysia’s economy has been roaring again, expanding by 5.1% y-o-y in 1H24. The momentum has also been impressive, hitting 2.9% q-o-q, seasonally adjusted, in 2Q. Beyond strong headline numbers, what is more encouraging is the breadth of the recovery.

For one, the long-anticipated revival in manufacturing is rather outstanding. Albeit delayed compared to peers, Malaysia’s manufacturing and trade sectors have finally turned the corner, riding the global tech upturn. After a long stretch of annual declines, electrical and electronics shipments returned to growth on a three-month moving average basis, albeit this remains at a nascent stage. Meanwhile, there is a mixed performance in commodities, with palm oil and LNG exports leading.

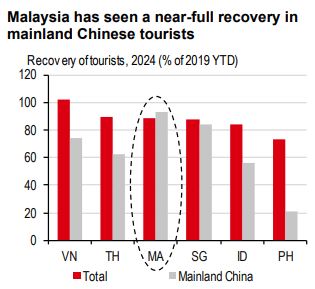

In addition to manufacturing, what was a great surprise is the performance of construction, which expanded by a double-digit y-o-y pace for the second consecutive quarter. Coupled with the expenditure side of the gross fixed capital formation data, this is not only related to the government’s recent increase in public investment but also reflects rising interest in FDI-related large-scale projects. Meanwhile, services continue to show strength. Not only has private consumption shown resilience, but tourism has also added much-needed fuel, as Malaysia has welcomed tourists equivalent to 90% of its pre-pandemic levels.

Given the upside surprise in 2Q, we recently upgraded our GDP growth for 2024 to 5.0% (previously: 4.5%), while keeping 2025 growth at 4.6%.

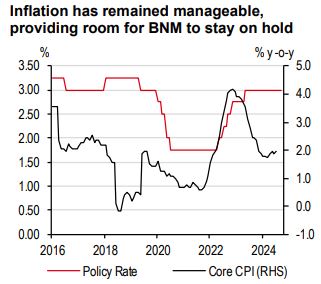

Outside of growth, inflation pressure remains largely muted, despite diesel subsidy rationalisation in June. Headline inflation averaged around 1.8% y-o-y in the first seven months of the year. Even after taking into account unfavourable base effects, we expect manageable inflation. We forecast inflation at 2.3% in 2024 and 3.0% in 2025, though acknowledge uncertainty from the potential subsidy rationalisation on the petrol RON95. Our base case is for Bank Negara Malaysia (BNM) to keep its policy rate steady at 3.0% for a prolonged period. As long as inflation falls within BNM’s 2-3.5% forecast range, we do not expect the central bank to move. That said, the risk of a hike is higher than a cut in Malaysia, compared to regional peers.

The Philippine central bank, Bangko Sentral ng Pilipinas (BSP), embarked on its easing cycle in August, cutting its policy rate by 25bp to 6.25% – even before the Federal Reserve (Fed) had lowered its policy rate.

It is good to look back to see how impressive this was. From 2022 to 2023, not only was inflation in the Philippines the highest in ASEAN, but the economy’s current account deficit was as wide as it was in the run-up to the Asian Financial Crisis. Many, including HSBC, thought that monetary policy in the Philippines had the least independence from the Fed when compared to others in ASEAN.

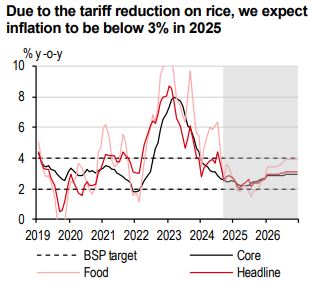

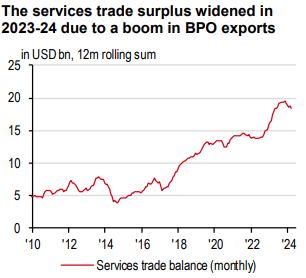

However, the Philippines in 2024 held itself together and turned the corner. The authorities cut the tariff for rice – the country’s most ubiquitous staple – from 35% to 15%, setting the stage for headline inflation to ease to below 3% y-o-y, or to within the lower bound range of the BSP’s 2-4% target band. The current account deficit is also moderating at a pace faster than expected, thanks to the economy’s Business Process Outsourcing (BPO) sector booming over the past year. This provides the BSP with inflows to help strengthen the peso and some support to wiggle away from the Fed. And, given how far inflation can still ease, the BSP already signalled that more rate cuts are to come.

The easing cycle comes at a good time. Although growth in the Philippines has held up relative to the

rest of Asia, some cracks are already showing. For instance, growth in household consumption dipped to its lowest level since the Global Financial Crisis, barring the COVID-19 pandemic, while growth in durable equipment investment has fallen for the second consecutive quarter. Credit in the economy also remains weak with the cost of borrowing high. That said, we expect the BSP’s easing cycle to reinvigorate small- to medium-scale investments and reduce the debt burden of households, bolstering growth in 2025 and 2026. We are even more bullish on next year’s prospects, with the tariff rate cut on rice potentially freeing-up 1.1% of the economy for growth.

With inflation on its way down but nothing terrible happening to GDP, we expect the BSP’s easing cycle to be gradual. We expect only one more 25bp rate cut (to 6.00%) in 2024 and pencil in a total of 100bp worth of rate cuts in 2025, bringing the year-end policy rate to 5.00%. We think the easing cycle will end in 2025, so we expect the policy rate to remain at 5.00% throughout 2026.

Singapore has made good progress in its economic recovery in 2024. While the possibility of a technical recession was still on the cards in 2Q23, the recovery momentum continues, helping Singapore to emerge from a severe downturn in the trade cycle to see healthy growth of c3% y-o-y in 1H24.

While manufacturing remained in contraction, the magnitude was much smaller, and it is also a mixed story. The culprit was falling pharmaceutical output, which is volatile in nature, and could swing back to growth later. Electronics output still saw a decent recovery, though the pace lags behind other tech-exposed economies like Korea and Taiwan Region. But this is because they have heavier exposure to Artificial Intelligence (AI)-related production, and Singapore is set to ride a broader recovery in consumer electronics.

Despite still subdued manufacturing activity, better-than-expected services came to the rescue. But it is also a mixed bag. On a sequential basis, domestically oriented sectors fared better, while consumer-facing and travel-related ones saw large corrections in 2Q. But this was largely expected, as a busy line-up of large-scale international concerts was concentrated in 1Q. That said, there is still potential to grow further. Singapore has welcomed visitors equivalent to almost 90% of 2019’s level in 1H24. July saw for the first time the return of Chinese tourists exceeding the monthly 2019’s level.

All in all, we recently upgraded our growth forecast to 3.0% (previously: 2.4%) for 2024 and maintain our 2025 growth forecast at 2.6%.

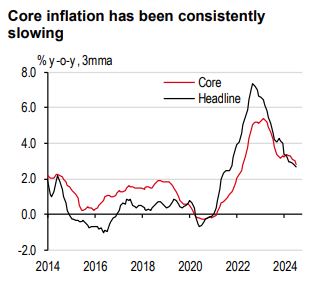

In addition, the disinflation progress also continues with core inflation decelerating to 2.5% y-o-y in July. Services inflation like education and healthcare continued to trend down, but entertainmentrelated costs barely budged. Most importantly, fuel and utilities cost momentum was muted, and oil prices are likely to stay relatively range-bound for now. As such, we recently revised down our core inflation forecast to 2.8% for 2024 (previously: 3.1%) and 1.9% for 2025 (previously: 2.2%).

Despite cooling inflation, we do not believe this will prompt the Monetary Authority of Singapore (MAS) to ease anytime soon; at least inflation trends on their own may not be enough to warrant an easing bias from the MAS.

Thailand’s GDP growth accelerated to 2.3% y-o-y in 2Q 2024, with its fiscal engines finally up and running, despite delaying the release of its budget for six months. The manufacturing production index in July also at last turned positive after falling for roughly 21 months, while goods exports leaped by 21.8% y-o-y as Thailand benefitted from the global tech upcycle. This coincides with the PMI new orders index, which just turned expansionary for the first time in 12 months back in July. All in all, it seems the economy is finally revving up. We expect Thailand to stage a V-shaped recovery for the remainder of 2024, growing 2.7% and 3.7% y-o-y in 3Q and 4Q 2024, respectively.

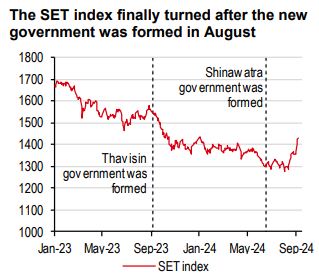

However, a lot happened before the economy got to where it is now. Amidst tough competition from mainland Chinese imports, headline inflation dropped back to below the Bank of Thailand’s (BoT) 1- 3% target band, while the trade balance swung back into deficit. Thailand also saw its political landscape change quickly: in less than 48 hours after Srettha Thavisin was removed from office, parliament elected Paetongtarn Shinawatra as Thailand’s youngest Prime Minister in history.

Although progress hasn’t been a straight line, the general direction is improving. In fact, amidst the political volatility, financial markets in Thailand finally ticked up after underperforming for 12 straight months. The SET index in September jumped for the first time this year, while the THB nominal effective exchange rate (NEER) is nearing its pre-pandemic levels.

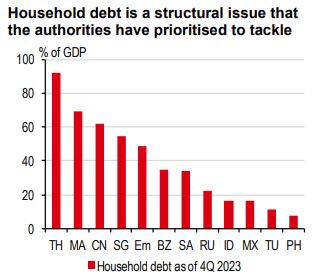

The Thai economy, however, isn’t all in the clear. Yes, government spending and tourism continue to fuel growth. But headwinds persist in manufacturing and consumption. Competition from mainland Chinese imports may limit how far manufacturing can improve while Thailand’s high household debt will likely be a major drag on private consumption.

That’s the complicated part. Although headwinds are strong and inflation is weak, we do not expect the Bank of Thailand (BoT) to ease monetary policy from now until 2027. Keeping the policy rate at 2.50% should help guide Thailand’s much-needed deleveraging cycle, particularly on household debt.

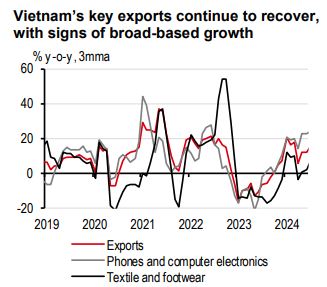

Vietnam’s economic recovery continues to firm up as the Year of the Dragon progresses. Growth improved and surprised on the upside in 2Q24, rising 6.9% y-o-y in 2Q24. The recovery in the external sector has started to broaden out beyond consumer electronics, although the pass-through to lifting the domestic sector still remains to be seen.

For one, the manufacturing sector has emerged strongly from last year’s woes. PMIs have registered five consecutive months of expansion, while industrial production (IP) has registered a bounce-back in activity for the textiles and footwear industry as well. This has supported robust export growth at double digits, with structural forces, such as expanding market access for Vietnamese agricultural produce, also underway.

However, the domestic sector is recovering more slowly than initially expected, with retail sales growth still below the pre-pandemic trend. Encouragingly, the government has put in place measures to support a wide range of domestic sectors that is expected to shore up confidence with time. Environment tax cuts on fuel and value-added tax cuts for certain goods and services will last until year-end 2024, while the revised Land Law effective from August will buttress the outlook for real estate. Albeit still early, the latter seems to have already contributed to a boost in foreign investment in the sector, with recent FDI showing broad-based gains.

We believe the potential upside risks can offset the temporary economic disruptions from Typhoon Yagi. All in all, we forecast GDP growth at 6.5% for both 2024 and 2025.

On inflation, price developments are turning more favourable in 2H24, as unfavourable base effects from energy have faded. An expected Fed easing cycle will also help to alleviate some exchange rate pressures. Taking all these into consideration, we forecast inflation at 3.6% in 2024 and 3.0% for 2025, both well below the State Bank of Vietnam’s target ceiling of 4.5%.

Additional disclosures

1. This report is dated as at 07 October 2024.

2. All market data included in this report are dated as at close 04 October 2024, unless a different date and/or a specific time of day is indicated in the report.

3. HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking, Principal Trading, and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

4. You are not permitted to use, for reference, any data in this document for the purpose of (i) determining the interest payable, or other sums due, under loan agreements or under other financial contracts or instruments, (ii) determining the price at which a financial instrument may be bought or sold or traded or redeemed, or the value of a financial instrument, and/or (iii) measuring the performance of a financial instrument or of an investment fund.

This document is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document is distributed by HSBC Bank Canada, HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank (Taiwan) Limited, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (200801006421 (807705-X)), The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank Middle East Limited, HSBC UK Bank plc, HSBC Bank plc, Jersey Branch, and HSBC Bank plc, Guernsey Branch, HSBC Private Bank (Suisse) SA, HSBC Private Bank (Suisse) SA DIFC Branch, HSBC Private Bank Suisse SA, South Africa Representative Office, HSBC Financial Services (Lebanon) SAL, HSBC Private banking (Luxembourg) SA and The Hongkong and Shanghai Banking Corporation Limited (collectively, the “Distributors”) to their respective clients. This document is for general circulation and information purposes only. This document is not prepared with any particular customers or purposes in mind and does not take into account any investment objectives, financial situation or personal circumstances or needs of any particular customer. HBAP has prepared this document based on publicly available information at the time of preparation from sources it believes to be reliable but it has not independently verified such information. The contents of this document are subject to change without notice. HBAP and the Distributors are not responsible for any loss, damage or other consequences of any kind that you may incur or suffer as a result of, arising from or relating to your use of or reliance on this document. HBAP and the Distributors give no guarantee, representation or warranty as to the accuracy, timeliness or completeness of this document. This document is not investment advice or recommendation nor is it intended to sell investments or services or solicit purchases or subscriptions for them. You should not use or rely on this document in making any investment decision. HBAP and the Distributors are not responsible for such use or reliance by you. You should consult your professional advisor in your jurisdiction if you have any questions regarding the contents of this document. You should not reproduce or further distribute the contents of this document to any person or entity, whether in whole or in part, for any purpose. This document may not be distributed to any jurisdiction where its distribution is unlawful.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/business. However, the Bank disclaims any guaranty on the management or operation performance of the trust business.

The following statement is only applicable to by HSBC Bank Australia with regard to how the publication is distributed to its customers: This document is distributed by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL/ACL 232595 (HBAU). HBAP has a Sydney Branch ARBN 117 925 970 AFSL 301737.The statements contained in this document are general in nature and do not constitute investment research or a recommendation, or a statement of opinion (financial product advice) to buy or sell investments. This document has not taken into account your personal objectives, financial situation and needs. Because of that, before acting on the document you should consider its appropriateness to you, with regard to your objectives, financial situation, and needs.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

Mainland China

In mainland China, this document is distributed by HSBC Bank (China) Company Limited (“HBCN”) and HSBC FinTech Services (Shanghai) Company Limited to its customers for general reference only. This document is not, and is not intended to be, for the purpose of providing securities and futures investment advisory services or financial information services, or promoting or selling any wealth management product. This document provides all content and information solely on an "as-is/as-available" basis. You SHOULD consult your own professional adviser if you have any questions regarding this document.

The material contained in this document is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HSBC India does not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investments are subject to market risk, read all investment related documents carefully.

© Copyright 2024. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks. In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.